Alex Harvey - Senior Portfolio Manager & Investment Strategist

Alex Harvey - Senior Portfolio Manager & Investment Strategist

Two months in, two regimes decapitated. With ten calendar months remaining for 2026 one wonders if there aren’t a few leaders of some questionable regimes mulling over their options right now. It’s not possible to reflect on February without jumping straight to the last day of the month which saw the rapid escalation of the US/Iranian nuclear talks stand-off. This culminated in the US and Israel launching joint missile attacks on Tehran, and Iran more widely, that led to the killing of the Ayatollah Ali Khamenei, the decades long spiritual leader of the Islamic Republic, and numerous of his senior personnel. This has led to a significant repricing of both risk assets and rates expectations, with the former reacting to the latter as oil prices spiked on fears that a closed Strait of Hormuz, and the ensuing restricted supply of crude oil and refined products, would wake inflationary concerns from their slumber. And wake them they have. March will likely offer up time for a more considered appraisal of just how that could play out in the months – or possibly even years - ahead.

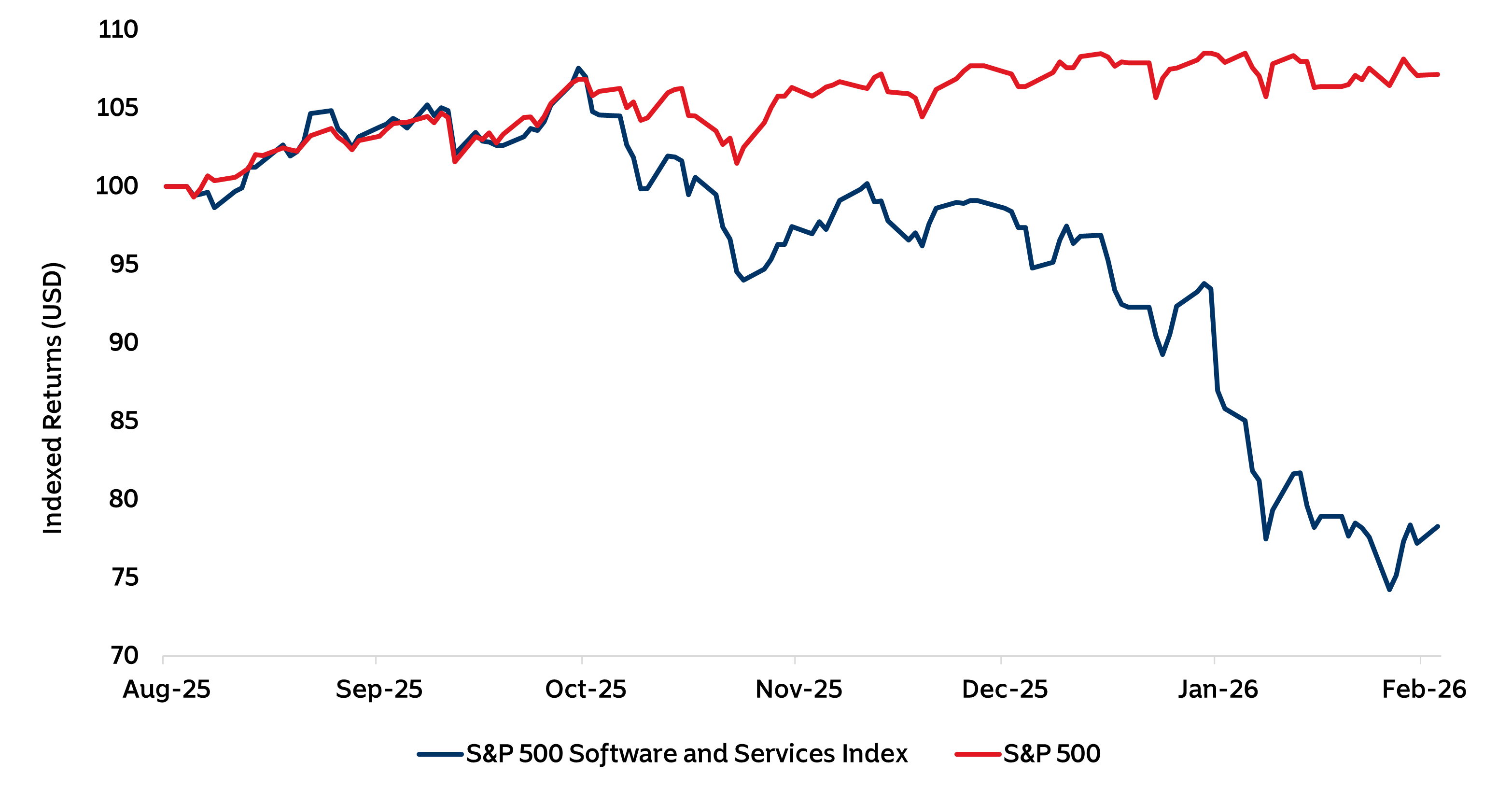

February started as January ended, with savage volatility in precious metals which all eventually ended the month in the green, with silver leading the charge up 18% after being down almost 10% at one point. Risk assets added at the top line, but it wasn’t a level playing field and the broadening out of equity returns theme continued as the US underperformed (it was one of the few developed markets down in absolute terms) and regional equity markets gained. Japanese equities added more than 10% and it wasn’t purely down to Yen weakness (it only gave up 1% against the dollar). Sanae Takaichi’s election gamble paid off handsomely and the majority victory was well received by investors who promptly bid up the local market. UK equities were up almost 7%, emerging markets over 5%, and European equities 3.5%. Stylistically, the markets rewarded value and low volatility stocks with growth equities posting another down month – its fourth on the trot – with the growth poster child ‘Mag 7’ index down 6.5%. February bore witness to the ‘SaaSpocalyse’ or ‘SaaSmageddon’ as it’s also been termed; a sharp decline in the price of software (as a) service stocks perceived to be most at threat of disruption – or extinction – from artificial intelligence (AI). We just don’t know at this stage how it will play out but the moves look extreme for a cohort of companies that retain a lot of intellectual property and valuable data that sits within their infrastructure and is not free to access for AI models. Whilst the moves may prove to be overdone, one could argue that the performance of ex-US markets and more value tilted equities is healthy.

‘SaaSpocalypse now’ - US software and services stocks fall

Source: Bloomberg Finance L.P., as of 2 March 2026.

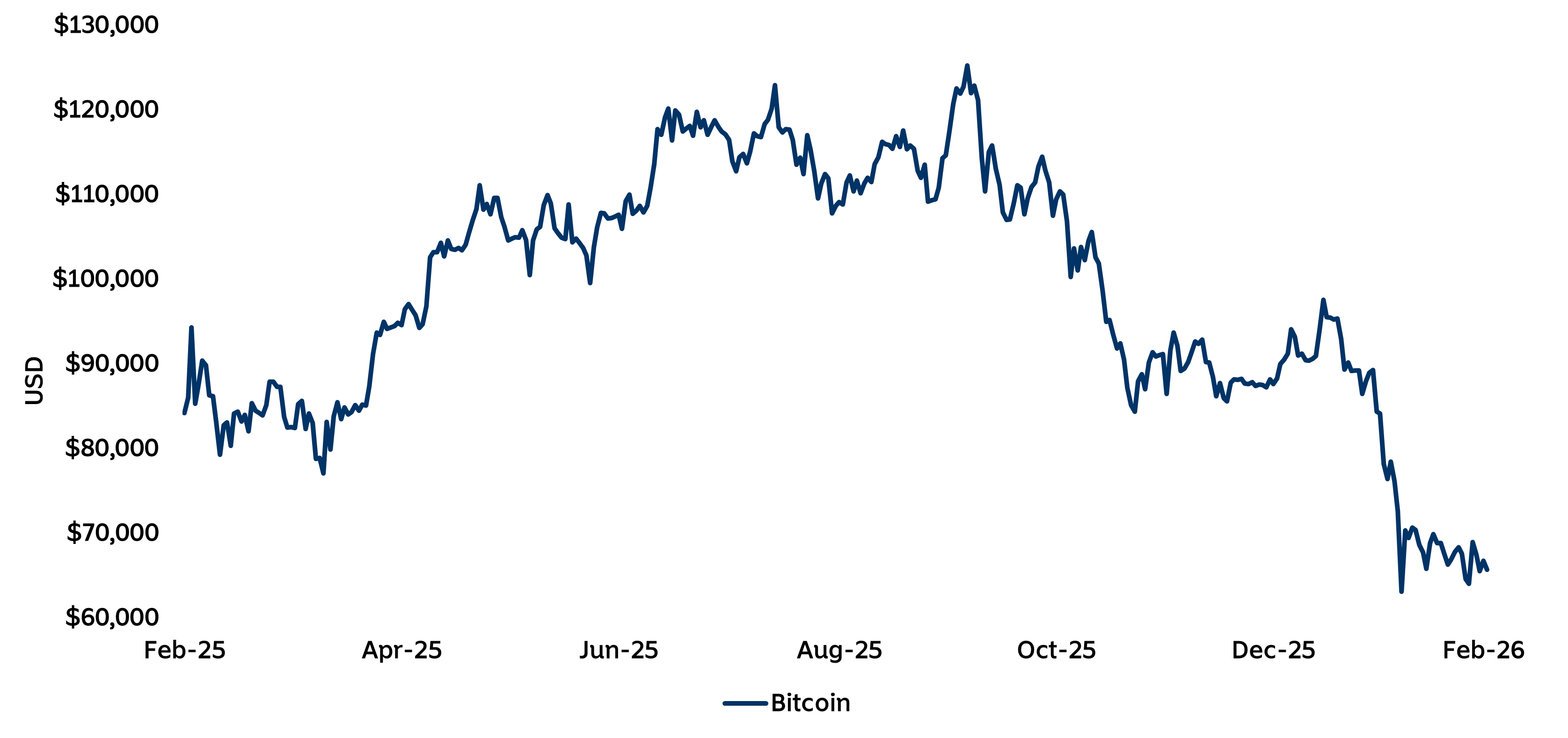

Some of the more surprising moves on the month were focused on the listed real assets space with global property and infrastructure adding 6% and 7% respectively. Arguably they could be perceived as something of a haven to more risky core equity assets, and they carry an implicit exposure to bond markets, which also posted positive returns in the low single digits. Alongside gold and other alternatives, this helped drive returns for more diversified multi asset portfolios. Bitcoin, and cryptocurrencies more broadly, had a torrid month. It was the fifth consecutive down month for the best known of the crypto assets, with Bitcoin falling 17% on the month, ending February almost 50% lower from its October high, wiping out all the gains and more since Trump returned to the White House with his pro ‘crypto bro’ agenda.

‘Crypto bro-ken?’ - Bitcoin falls nearly 50% from peak

Source: Bloomberg Finance L.P., as of 27 February 2026.

In terms of the data behind the market performance, growth in the US in Q4 was down from the prior quarter, but still ahead of most of Europe and the UK, which itself only mustered a 0.1% quarterly growth in output. The labour market continues to soften, and the Federal Reserve continues to focus attention there for now when considering the path of future rates. Rates were held in the UK and Europe but given the seismic shift in the outlook for inflation expectations following the advent of the Middle East military escalation, we would expect that all rate cuts are off the table at present.

We find ourselves wrapping up what we could describe in the end as a relatively healthy month for mainstream financial assets and those with a supportive valuation grounding. But it has also exposed vulnerabilities in industries perceived as being safer, in part because of their asset light balance sheets, which has attracted private capital in recent years, some of which now wants an exit and has led to some vehicles restricting redemptions. This comes at a time of heightened geopolitical risk, with attention focused squarely on a strip of water some 21 miles across. The ‘distraction’ of Iran arguably plays into the hands of those with issues closer to home, be that east or west, and to the detriment of existing parties that risk being deprived of both physical firepower and media coverage. It also draws in other global players with vested interests in seeing the Strait of Hormuz stay open, as the big energy importers may be forced to look for sanctioned supplies or alternative energy sources such as American LNG (liquified natural gas). Undoubtedly this is a time for caution as the risk of a more protracted conflict mounts, as this would have a material impact on global growth and inflation. This does not immediately feel like the kind of ‘buy the dip’, ‘Trump always chickens out’ (TACO) opportunity that presented on several occasions last year. Our multi asset portfolios remain well diversified, overweight quality, with moderate to underweight interest rate exposure versus strategic benchmarks.